Here’s a piece of really good news for you. If you are reading this, you are already taking your first step toward debt relief. Finding out what you can do to get debt help is a positive action that can lead to long-term success.

The stronger your desire to take control of your debt, the more likely you will be to take appropriate steps to become debt-free. There are just six steps to successful debt resolution.

Taking steps to understand your financial situation can help you decide whether you need professional debt relief or whether you can work your way out of debt by budgeting more carefully and practicing good money management skills.

The time it takes to get out of debt is dependent on several factors, including, but not limited to:

In general, you should plan on spending anywhere from 2 to 5 years to become completely debt-free.

Get a free savings estimate today to see how much you can save.

If you don’t want to run the risk of getting a secured loan to consolidate your debt, you may be thinking of a balance transfer for credit card consolidation instead.

Here’s what you should know about balance transfers and debt relief. Using a balance transfer is, in reality, just paying off one credit card with another credit card. So, ultimately, you will need to address the larger problem of how to exercise good financial discipline to make a balance transfer really work in your favor.

That said, there are some circumstances in which a balance transfer may work. Here are the things that must be true for a balance transfer to be a good deal for debt relief:

Assuming you can find a card that meets those criteria, a balance transfer may be an option for you. Here’s a look at a scenario in which a balance transfer could work.

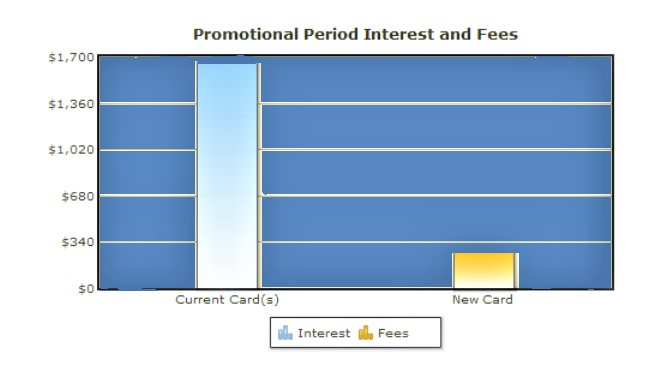

Suppose you have two credit cards. On card one, you owe $5,000 and your APR is 16.49%. On card two, you owe $4,500 and your APR is 18.49%. You have excellent credit and you find a balance transfer offer with an introductory APR of 0% for 12 months and 16.49% thereafter. The card provider will charge a 3% transfer fee upfront. Is this a good deal?

(Source: Motley Fool)

By transferring your credit card balances and not charging anything else to your credit cards, you can save an extra $1,372 over the next 12 months and then save $7 per month after the introductory period ends.

Sounds good, right? It is, with one caveat. It only works like that if you do not continue to use your credit cards, either for purchases or for cash advances.

If you can stop making purchases on your credit cards completely, this balance transfer option may help you get out of debt. It does not, however, reduce the total amount you owe. It may simply help you pay down your debt by reducing the interest that you pay over time.

Debt settlement is a debt relief option that involves working with your creditors to create a debt reduction plan. It is different from a debt management plan in that, with debt management, you are still paying your creditors the full amount of your debt. With debt settlement, on the other hand, your creditors are making an agreement with you to accept less than what you owe to them.

You may wonder why creditors would agree to accept less than what you owe. The simple answer is that, when a person is experiencing financial hardship and having real trouble paying bills, creditors are aware that it is quite possible that they will be unable to recoup any money if the person declares bankruptcy. So, to avoid the possibility of getting none of their investment back, your creditors may be willing to negotiate a settlement to ensure they recoup at least some of their money.

That is not to say that creditors will make this decision lightly. For this reason, most people who choose to try debt settlement do so with the help of a debt settlement company that specializes in negotiating with creditors on behalf of their clients.

Here’s how it works:

Call a ClearOne Advantage Certified Debt Specialist at 866-481-1597. During that brief phone call, your debt specialist will learn about your unique debt situation and talk with you about your options for debt settlement. If it seems like a good fit, you will get a savings estimate and customized debt settlement plan that you can review.

Once you decide on which plan fits you best, you will set up an escrow account and begin making payments to the account. Once sufficient funds have accumulated in your escrow account, our skilled negotiators start the process of negotiating with your creditors. And there are no upfront fees to get any of this done.

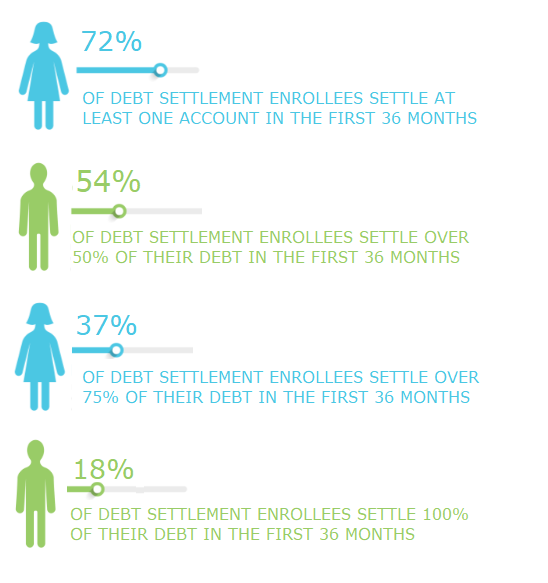

Although it may sound too good to be true, debt settlement does work. According to a 2020 report commissioned by the American Fair Credit Counsel, total debt settlement program savings average just under $5,800 after fees, and for every $1.00 spent on debt settlement fees, individuals receive an average of $2.67 in debt reduction. The report also revealed the following statistics regarding the success rates of debt settlement programs:

Debt settlement is the only debt relief option other than bankruptcy that enables you to actually pay less than you currently owe to get out of debt. If you are struggling with a heavy debt load, it is a smart move to consider debt settlement as a viable option.

Now that you are aware of your debt relief options, what is your next step? Why not talk with a Certified Debt Specialist who can answer your questions, discuss your unique situation, and design a customized plan to help you get out of debt within 24-60 months? Call 866-481-1597 to get a free savings estimate today.

The information provided is for informational purposes only and is not intended to provide legal or financial advice. ClearOne Advantage is not a lender, credit repair or consumer credit counseling company. ClearOne Advantage doesn’t provide investment, tax or legal advice. Please consult a certified financial advisor for individual credit and lending advice. Please consult with a bankruptcy attorney for more information on bankruptcy.

410 N Scottsdale Rd

Suite 1000

Tempe, AZ 85281

©2024 ClearOne Advantage, All rights reserved.

ClearOne Advantage is a registered service mark of

ClearOne Advantage LLC.