Whether it's trying to maintain a certain lifestyle or prove your worth to others, it's easy to overspend. It's especially easy to stretch your financial limits in a society that encourages consumerism. Here are some of the most common reasons for overspending, along with some tips about what you can do to avoid these debt traps.

1. Impulse Shopping

The easiest purchases to regret are often the ones you didn't plan for. Retailers are designed to encourage unplanned buying, from product placement to limited-time offers. It's easy to leave the store having spent more than you intended.

A few simple habits can help you stay on track:

- Write out a list before you go shopping and stick to it

- Set a budget for each trip and bring only what you plan to spend

- Give yourself a 24-hour pause before buying anything that wasn't on your list

Small adjustments like these can add up to real savings over time.

2. Letting Small Expenses Add Up

It's easy to feel the impact of a big purchase. But smaller, everyday spending is a different story. A coffee here, a rideshare there, a few nights out. None of it feels significant in the moment, but it can quietly eat into your budget over time.

Tracking everything you spend, even the small stuff, can be an eye-opening exercise. Most people are surprised by how quickly incidental expenses add up once they see them written down. And once you see the pattern, it's a lot easier to decide where you actually want your money going.

3. "Keeping up with the Joneses"

Social pressure around money is real, and it shows up in big ways and small ones. FOMO plays a bigger role in spending decisions than most people realize It might look like stretching to afford a house or car that signals a certain lifestyle. Or it might be as simple as picking up a tab, joining a trip, or going out when your budget says otherwise.

This isn't a character flaw. It's a pattern a lot of people find themselves in, and it's worth being honest with yourself about where social expectations are driving your spending decisions.

The good news is that the relationships that matter most don't require a lot of cash to maintain. People who genuinely care about you aren't keeping score of your car, your house, or what you pick up at dinner. And when you're upfront about your budget, the people worth keeping in your life will meet you with understanding instead of judgment.

Related: Should You Go Into Credit Card Debt to Travel?

4. Not Having a Budget

A budget isn't about restricting yourself. It's about knowing where your money is going so you can make deliberate choices about it. Without that clarity, it's easy for unplanned purchases to slip through, not because you're careless, but because you're working without a complete picture.

Getting started doesn't have to be complicated. Even a simple breakdown of your income and regular expenses can shift the way you think about spending. When you know what you have and where it's going, every purchase becomes a choice rather than a reflex.

ClearOne Advantage has a number of resources to help you get started. Once you have a created a budget, the goal is consistency, not perfection. Small, steady progress adds up over time.

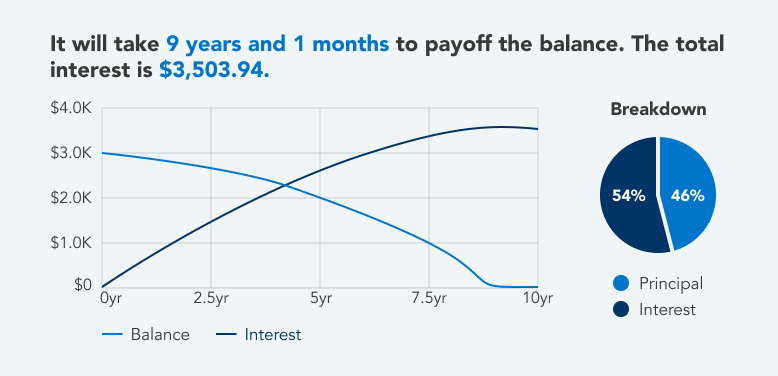

5. Costs Associated with Being in Debt

Most people know they're paying interest on their balances, but the full picture is easy to underestimate. On a credit card with a 20% APR, a $3,000 balance that you're only making minimum payments on can end up costing you significantly more than that over time, and take years to pay off.

There's also an opportunity cost. Money going toward interest every month is money that isn't going toward savings, an emergency fund, or anything else that moves you forward financially.

Related: How to Avoid the Minimum Payment Trap

6. Living for Right Now

It's human nature to prioritize what feels good today over what's better for you tomorrow. Psychologists call this present bias, and it affects everyone to some degree, not just people in debt.

The challenge is that small, feel-good spending decisions in the moment can quietly work against your longer-term financial picture. The good news is that you don't need a complete mindset overhaul to shift this. Focusing on small, concrete goals such as paying down one balance, building a one-month emergency fund tends to be more effective than trying to think decades ahead.

7. Shopping as a Coping Mechanism

Retail therapy is real. For a lot of people, spending money is a way of managing stress, anxiety, or difficult emotions. There's nothing unusual about that. The challenge is when it becomes a pattern that works against your financial goals.

If you notice that shopping tends to follow hard days, big emotions, or stressful situations, it's worth paying attention to that connection. It doesn't mean something is wrong with you, it means you've found a coping mechanism that has a financial cost attached to it.

For some people, talking to a financial counselor or therapist can help untangle the emotional side of spending. For others, having a clearer picture of their finances is enough to shift the pattern.

Work with ClearOne Advantage

The strategies above can help you stop debt from growing, but if you're already carrying a balance that feels hard to manage, that's a separate conversation. There are debt relief options worth exploring. Contact a ClearOne Certified Debt Specialist at 888-340-4697 or get a free savings estimate.