What is Credit Counseling?

If you are looking for a way to get out of credit card debt and regain your financial freedom, one of the options you may be considering is credit counseling. Here, we'll explore what credit counseling is, how it works, and if you have a considerable amount of debt, why it may not be the best option when compared to the benefits offered by debt settlement.

What Is Credit Counseling?

Credit counseling offers advantages similar to debt consolidation loans because it combines credit card debt into a single, lower-cost bundle. Unlike debt consolidation loans, however, credit counseling does not require you to qualify for a loan. Therefore, you do not need a good credit score to qualify for credit counseling.

Through this debt resolution method, you hand over the management of your debt to a credit counseling agency (CCA). You pay the CCA and they deal directly with your creditors. The goal of the CCA is to get you reduced interest rates and penalty forgiveness from your creditors.

Your debt management plan (DMP) payment is usually not much lower than you were already paying to your creditors, but the reduced interest rates usually allow you to pay off your creditors in four to five years. If you have a large amount of debt and are already struggling to make your monthly payments, the payment on a DMP may also put a strain on your budget.

In that case, you may want to consider a debt settlement plan, which takes into account what you can afford to pay. If you are not sure how to determine what you can reasonably afford to pay, you should discuss this with a ClearOne Advantage Certified Debt Specialist. They can help you by performing a free debt analysis which will let you know what your payment on a debt settlement plan could be and how quickly you can expect to resolve your debt based on your situation.

How Does Credit Counseling Work?

If you have credit card debt and you decide to go down the road of credit counseling, your first step is to shop for a credit counseling agency. Here are some factors you need to keep in mind about how debt management plans (DMPs) with credit counseling agencies work.

Before agreeing to work with a credit counseling agency, you will need to compare plans because the administrative costs can vary.

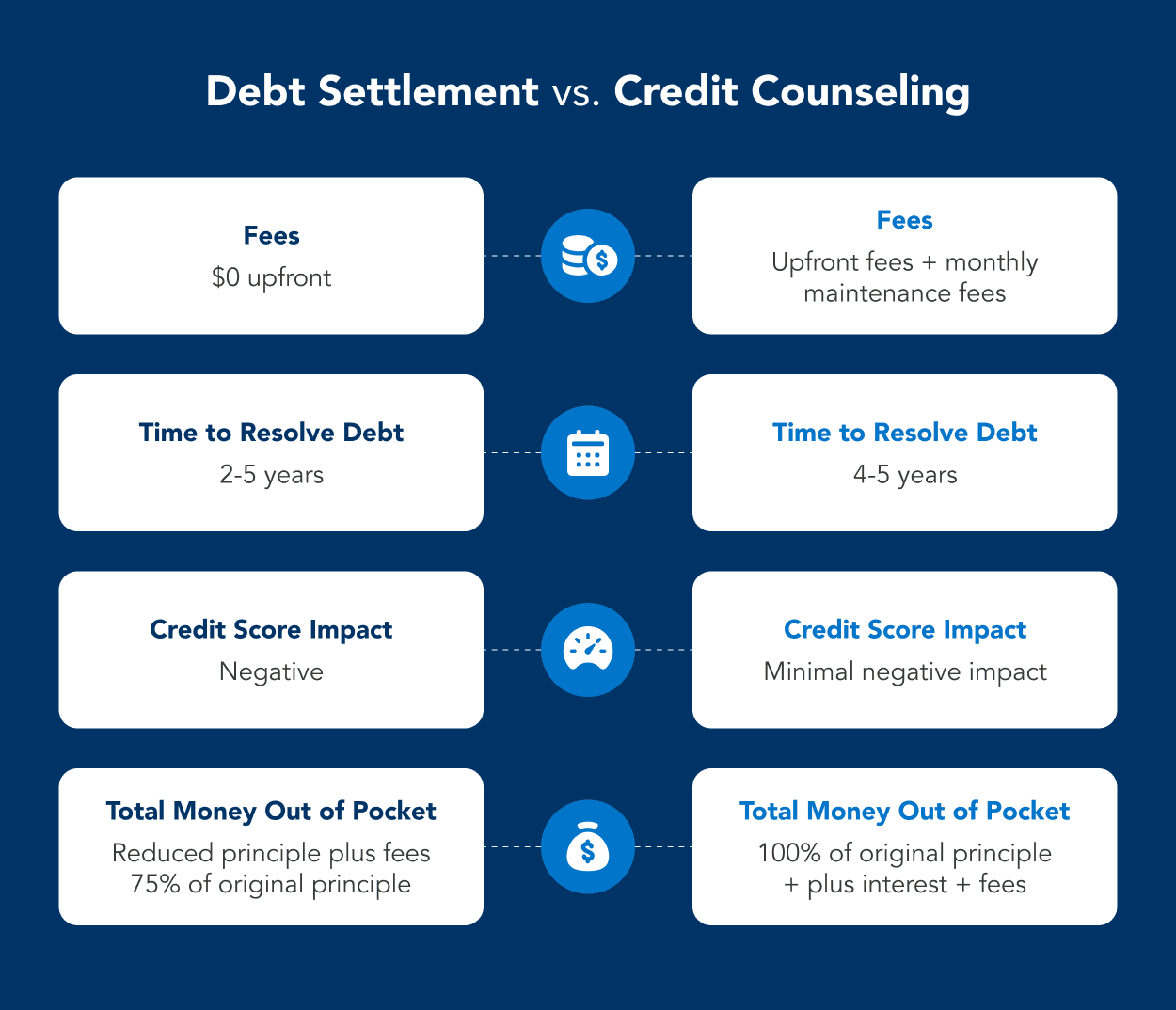

- Your DMP involves an upfront cost of around $75. This is how much it costs you to set up the plan. Other costs include your monthly service charges, which can range from $24 to $55 per month.

- Following your enrollment, you will make one payment to the CCA every month. From here on out, you will not deal directly with your creditors. The CCA will use those funds to repay your debts and collect its fees.

- CCAs have agreements with most credit card issuers, so you are usually safe from legal action once enrolled.

- A typical DMP can last three to five years. During this time, your credit report carries a notation specifying that you are participating in a debt management plan. Credit counseling can have a negligible impact on your credit score.

The benefits of credit counseling include lower interest rates and penalty forgiveness. Normally, you cannot expect any accrued interest to be forgiven. If you fail to complete the terms of your DMP, your lenders can claim your full debt balance regardless of the payments you made through the DMP.

Is Credit Counseling a Good Idea?

Credit counseling can provide you the right credit card relief solution if:

- You aim to retire credit card debt only.

- You do not qualify for other forms of debt consolidation.

- You earn enough money to keep up your DMP payments.

Below we will compare how DMPs differ from debt settlement plans. One of the major differences is that CCAs will not re-negotiate your debt to reduce your principal.

Advantages of Credit Counseling

- During your participation in the plan, you cannot open new credit cards and your credit report bears a DMP notation. After you graduate, however, you may be able to restore your credit rating quickly.

- A DMP allows you to repay your debts with reduced interest rates and fees.

- Credit score is not a factor for credit counseling qualification.

Disadvantages of Credit Counseling

- There may be upfront fees to pay in addition to monthly service fees.

- You are prohibited from opening new credit cards for the duration of the DMP.

- Discontinued DMPs do not discharge any debt. If you terminate your plan, be prepared to face the collection efforts of your creditors again.

- According to a report sponsored by the National Foundation for Credit Counseling, the odds of completing a DMP are statistically only 54 percent.

How does Credit Counseling Compare to Debt Settlement?

Debt settlement is the only debt relief method that can eliminate a part of the principal amount you owe. ClearOne Advantage's goal is to get creditors to accept less than the full balance owed on the debt - typically 50 percent.

Your debt settlement plan (DSP) will only include debts that are likely to be settled at a significant discount.

Is Debt Settlement Right for You?

Debt settlement enables you to pay less money to achieve freedom from the stress of debt. ClearOne Advantage can help you evaluate all your debt relief options to find the one that is right for you. Our Certified Debt Specialists help people find their way out of debt every day, and it starts with a free savings estimate. Defeat your debt the smart way. Find out how.