Paying the minimum on your credit card keeps your account in good standing, but it barely touches your balance. Most of your payment goes toward interest, which means balances can take a decade or more to pay off and cost you far more than you originally borrowed.

You open your credit card statement. The balance is $3,000. The minimum payment due is $60. You pay it, feel like you handled it, and move on.

The minimum payment isn't there to help you get out of debt. It's there to make $3,000 feel like a $60 problem.

What Is a Credit Card Minimum Payment?

Your minimum payment is the smallest amount your credit card issuer requires you to pay each month to keep your account current and avoid late fees. As long as you make this payment on time, your account stays in good standing and no penalty fees are added.

That's all it does. It keeps your account current. It doesn't meaningfully reduce what you owe.

Most credit card companies calculate your minimum as 1–2% of your outstanding balance, plus any interest and fees that accrued during the billing cycle. On a $3,000 balance, that works out to about $60.

What Is the Minimum Payment Trap?

The minimum payment trap is what happens when making only the required payment each month leaves you stuck. You're paying regularly but barely making progress on what you owe.

Here's how it works: on a $3,000 balance at 20% APR, your $60 minimum payment breaks down like this:

- Monthly interest charge: roughly $50

- Amount reducing your actual balance: about $10

You paid $60 and your debt went down by $10. Next month the same thing happens. And the month after that.

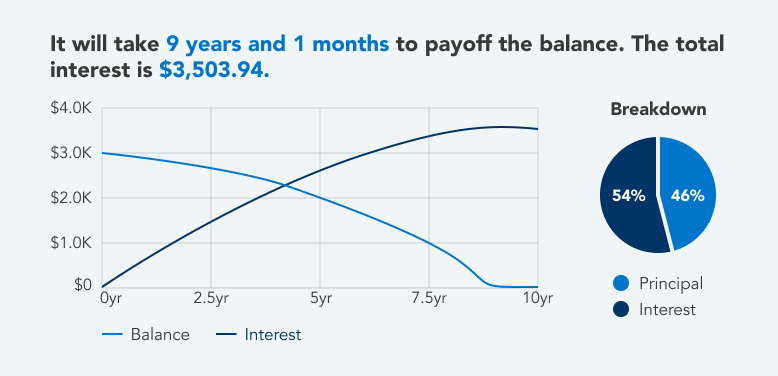

At that rate, it takes over 9 years to pay off a $3,000 balance. By the time you’re done, you’ll have paid approximately $6,503.94 total. That means about $3,503.94 of that was interest on a $3,000 purchase.

Source: Calculator.net

The trap is this: you can make every single payment on time, never miss a month, and still watch your balance barely move for years.

Does Paying the Minimum Avoid Interest?

No, paying the minimum does NOT avoid interest. This is one of the most common misconceptions about credit cards. Paying the minimum keeps you from being charged a late fee and keeps your account in good standing, but you're still charged interest on the remaining balance every single month.

Why the Trap Is So Easy to Fall Into

When you open your statement, the minimum payment is bolded, boxed, and front and center. Your brain latches onto that number before it fully processes the total balance sitting above it. A $60 payment feels manageable. A $3,000 balance feels overwhelming. So without realizing it, you start thinking about the minimum as what you owe that month and not as a small fraction of your balance.

That's the anchoring effect at work. Credit card companies know that the first number you focus on shapes how you respond. A low minimum lowers your sense of urgency, even when your balance is barely moving.

How to Avoid the Minimum Payment Trap

Look at the total balance on your statement, not the minimum

Before anything else, make checking your total balance a habit. The minimum payment is designed to be the number your eye goes to first. Ignore it. Look at the total balance and let that be the number that drives your decisions each month.

Pay more than the minimum, even a little

Even a small increase makes a real difference. Here's what that looks like on the same $3,000 balance at 20% APR:

| Monthly Payment | Time to Pay Off | Total Interest Paid |

|---|---|---|

| $60 (minimum) | 9 years, 1 month | $3,504 |

| $80 | 5 years | $1,747 |

| $100 | 3 years, 6 months | $1,193 |

Source: calculator.net

Paying $100 a month instead of $60 cuts more than 6 years off your payoff timeline and saves over $2,700 in interest.

Automate a payment above the minimum

One of the simplest ways to make consistent progress is to set up autopay for a fixed amount higher than the minimum. This removes the monthly decision about how much to pay and makes sure you're always chipping away at the principal. Even automating $80 or $100 a month instead of the minimum puts you on a meaningfully faster track without requiring willpower every billing cycle.

Use the avalanche method

With the debt avalance method, you list all your credit cards by interest rate, highest to lowest. Put any extra money toward the card with the highest rate while paying minimums on the rest. Once that card is paid off, roll that payment into the next one. This approach saves the most in interest over time.

Use the snowball method

The debt snowball method has you List your cards by balance instead, smallest to largest. Pay off the smallest balance first, then move to the next. You'll pay slightly more in interest overall compared to the avalanche method, but the early wins make it easier to stay on track.

Look into a balance transfer

Some credit cards offer 0% intro APR on balance transfers for 12–21 months, which means every dollar you pay during that period goes toward the principal rather than interest. Balance transfer fees typically run 3–5% of the amount you move over.

That said, this option isn't available to everyone. According to Bankrate, the best balance transfer cards generally require a credit score of at least 670, and issuers also look at your debt-to-income ratio. A DTI above 35% can work against you. If your credit has taken hits from carrying high balances or missed payments, you may not qualify for the cards with the most favorable terms.

What If You Can't Pay More Than the Minimum Right Now?

This is the situation a lot of people are actually in. If your budget genuinely doesn't have room to pay more, advice about budgeting harder or picking up extra income only goes so far.

If you've been making minimum payments for a while and your balances aren't moving, that's a sign the DIY approach may not be enough. Debt relief options like debt settlement or a debt management plan exist specifically for this situation. They're a practical tool for people whose debt has reached a point where the math no longer works in their favor.

ClearOne Advantage works with people in exactly this situation. Our Certified Debt Specialists can walk you through what your options actually look like and help you figure out whether a structured plan makes sense for your situation.

Free, No-Obligation Debt Analysis

See how much you could save. Call us today at 888-340-4697 or get a free, no-obligation savings estimate today.

Frequently Asked Questions

What is the minimum payment trap?

The minimum payment trap is when you make only the required monthly payment on your credit card, which mostly covers interest and barely reduces your balance. Over time, you end up paying far more than you originally borrowed and staying in debt much longer than necessary.

What is a credit card minimum payment?

It's the smallest amount your credit card issuer requires you to pay each month to keep your account in good standing and avoid late fees. Most issuers calculate it as 1–2% of your outstanding balance plus any interest and fees that accrued during the billing cycle.

Does paying the minimum payment avoid interest?

No. Paying the minimum keeps you from being charged a late fee, but you're still charged interest on the remaining balance. The only way to avoid interest entirely is to pay your full balance each month.

Why is it more difficult to get out of debt when only paying the minimum payment?

Because most of your minimum payment goes toward interest, not your principal balance. On a $3,000 balance at 20% APR, only about $10 of a $60 minimum payment actually reduces what you owe. The rest covers that month's interest charges.

Is it ever okay to just pay the minimum?

In a genuine short-term pinch, yes. Missing a payment is worse than paying the minimum. The problem is making it a habit. Over time, minimum payments mean you'll pay significantly more for every purchase and stay in debt much longer than necessary.

What happens if I can't make the minimum payment?

You'll typically be charged a late fee and your interest rate may increase. After 30 days, the missed payment may be reported to the credit bureaus. If you're struggling to meet minimums, it's worth exploring debt relief options before your situation gets harder to manage.

How can I make sure I never miss a payment?

Set up autopay through your credit card issuer for at least the minimum each month. Better yet, automate a fixed amount above the minimum so you're consistently making progress on your balance without having to think about it each billing cycle.