Credit Card Debt Relief

If credit card debt is taking a toll mentally, physically, and emotionally, you don't have to keep carrying that stress on your own. There are debt relief options available that will help you take control over your finances. Learn more about these options and which debt relief option may be right for you. Here's what you will learn as you read on:

- Do I need credit card debt relief?

- Common causes of credit card debt

- How does it work?

- Saving with debt settlement

- Timelines for settling your debt

Credit Card Debt Relief: Know When You Need It

You don't have to wait to hit rock bottom financially before getting help. In fact, if you are starting to feel that your credit card debt is a problem, it's better to be proactive in seeking help than waiting until it becomes completely unmanageable. Here are a few signs that you may be struggling with debt:

- You have trouble paying your bills on time: You may be able to pay some bills on time, but you may also miss payments and find yourself accruing late fees or higher interest rates.

- Calls from creditors or collectors: You may be receiving calls from creditors or collections agencies and feel unsure of what to say or how to handle them.

- Impacts to your well-being: Worrying about your debt interferes with your daily life, affects your focus, or causes you to lose sleep.

- Budgeting becomes difficult: You find it impossible to stick to your budget and feel like you're dealing with debt every day as you spend more than you earn.

- Retail therapy: Even though you worry about debt, you find yourself shopping as a way to cope with stress or feel better.

- Credit impacts:The amount of debt you're carrying has affected your credit, limiting other financial options that might otherwise be available.

- Shame or fear of judgment: You feel embarrassed about your debt and try to hide it from friends or family.

- A sense of hopelessness: You feel like no matter what you do, getting out of debt seems impossible.

If these sound familiar, please reach out to a ClearOne Advantage Certified Debt Specialist to talk about your debt relief options today at 866-481-1597.

Causes of Credit Card Debt

There are a lot of reasons people go into credit card debt. In many cases, debt is the result of rising costs, unexpected expenses, or gaps between income and necessities, not a personal failing.

The leading causes of credit card debt are:

1. Inflation and the cost of living

Rising prices can be a major reason people lean on credit cards. Even when wages increase, essential costs like housing and transportation can rise faster, according to Nerdwallet's 2025 Household Credit Card Debt Study. When these costs rise faster than wages, many families end up using credit cards just to cover basics like groceries, gas, and utilities.

2. Medical Expenses

Healthcare costs have risen significantly over the past few decades, and medical needs can strain your budget. As a result, some people use credit cards to pay for medical expenses directly, or to cover everyday necessities when medical costs take up a larger share of their income.

3. Impulse Shopping

Credit cards can make spending feel easier because you don't see money leaving your account right away. And with marketing designed to turn “wants” into “needs,” it's easy to overspend, especially on things that aren't truly necessary.

4. The Cost of Debt

Once you're carrying a credit card balance, interest can add up quickly, making it harder to make real progress against your debt. Even when you are making minimum monthly payments, it can feel like you aren't making progress. For example, if someone owes $10,000 at 18% interest and pays $200 per month (without charging anything new), it would take about 7 years and 10 months to pay it off, costing roughly $8,622 in interest alone.

5. Vacations and Home Improvement Projects

Vacations and home improvements can be debt traps for high-income earners. Because of their good credit scores, they may have higher credit limits that make it easy to overspend on high-dollar categories.

6. Unexpected Emergency Expenses

According to the Federal Reserve, 37% of Americans do not have enough savings to handle an unanticipated expense of $400 or more, including car or appliance repairs. Considering that a study by AAA revealed that the average cost of a car repair is $419, many are one car repair bill away from going into credit card debt.

How Does Credit Card Debt Relief Work?

There are several ways to obtain credit card relief. A ClearOne Certified Debt Specialist can help you figure out which of these options suits your particular situation the best.

- Debt consolidation loans bring your credit card debt under the roof of a single loan. To consolidate your credit, this loan will preferably feature a lower interest rate than what you are currently paying to your creditors to help you pay off your debt more efficiently.

- Credit counseling combines your debts into a single bundle, lowering the cost of your credit. It instills some much-needed discipline in your finances.

- Bankruptcy may be a solution if you are buckling under the burden of your credit card debt. This credit card relief method uses a legal avenue that allows you to discharge some of your debts while paying off the rest in a structured, disciplined way.

- Debt settlement is a form of credit card relief in which you work with your creditors toward a realistic debt reduction plan. In most cases, it is best to do this with the help of a debt settlement company that uses professionals to negotiate with your creditors on your behalf. Through debt settlement, your creditors may forgive a portion of your principal debt so you end up paying less than you owe. Contact ClearOne Advantage to learn more about how debt settlement works.

How Much Can You Save with Debt Settlement?

Creditors are often willing to make considerable concessions through debt settlement. Through debt settlement, they can recover money from debtors they could not get back otherwise.

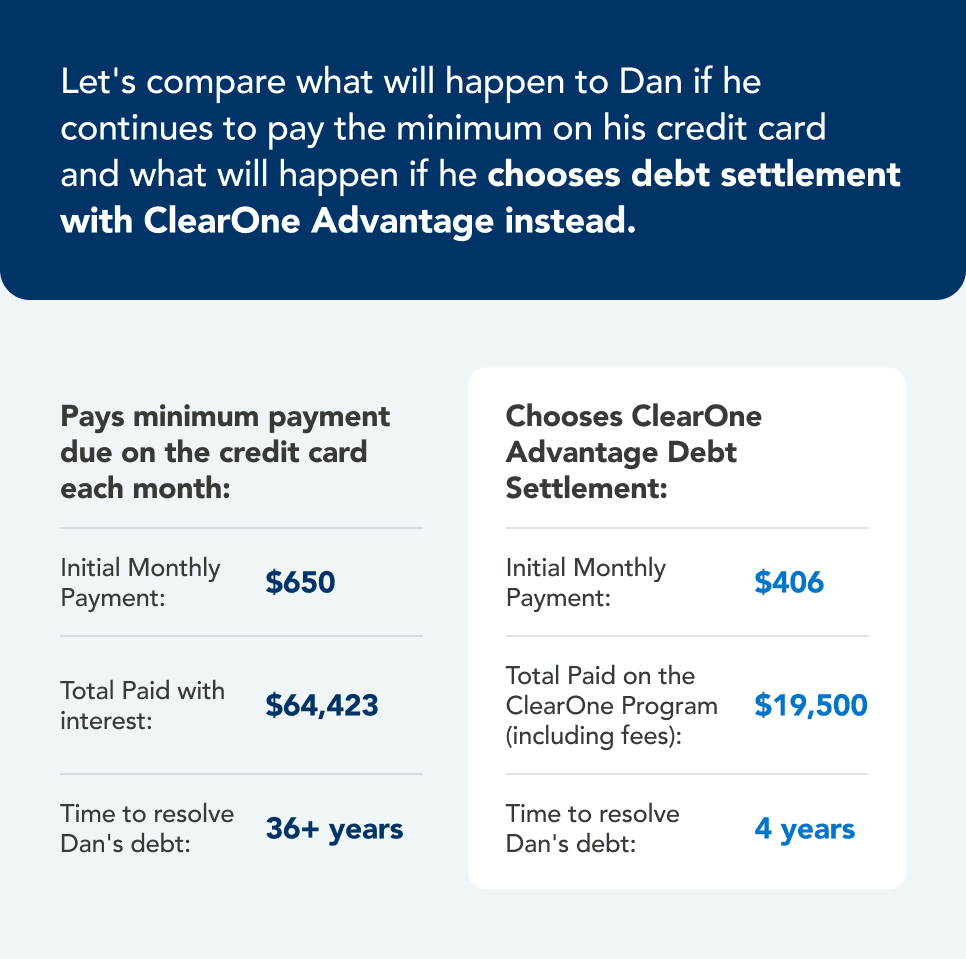

How much can you save with debt settlement? To illustrate, consider Dan's story.*

Dan works hard every day and has always been conscientious about paying his bills on time.

Unfortunately, Dan had an accident last year and the medical bills mounted up quickly. Dan paid his medical bills with a credit card, expecting to use money from an insurance settlement to pay the card off before it became a problem.

The settlement did not come through, and now Dan is struggling to pay the minimum payment each month on a credit card with a balance of $26,000 and an interest rate of 18%.

*“Dan” is an example of a typical ClearOne client, whose experience is a combination of the thousands of clients who are in the ClearOne program.

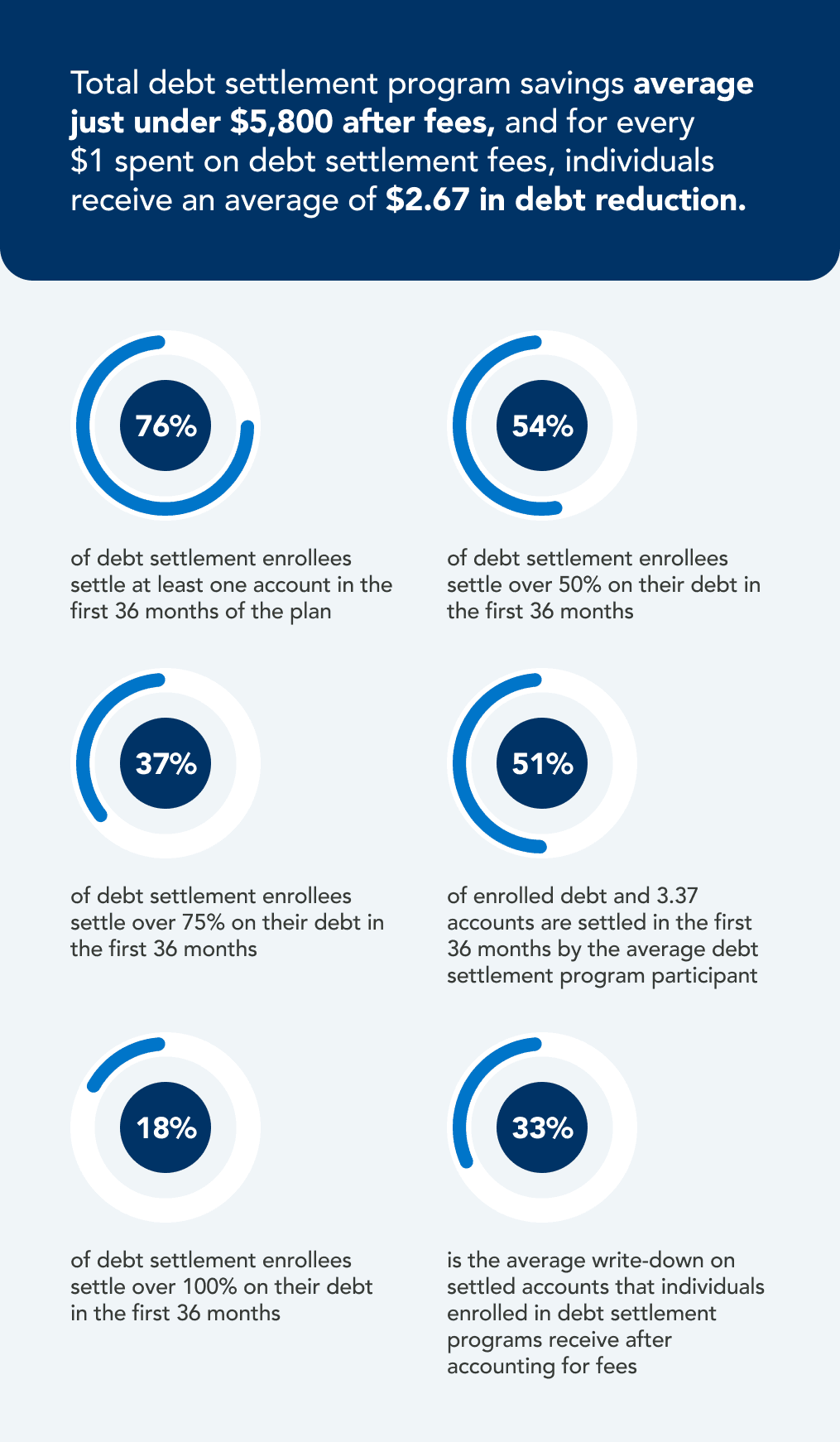

This is just one example, but it reflects the overall reality of debt settlement. According to the a study from the Harvard Kennedy School:

How Long Does it Take to Settle Credit Card Debt?

According to a study from the Harvard Kennedy School, 76% of those who enroll in a debt settlement program settle at least one account in the first 36 months of the plan, and 54% settle more than half of their debts in 36 months. The average debt settlement enrollee settles around 51% of his/her debt in the first 36 months.

How quickly you can resolve your debt depends on your income and the amount of money you can allocate to debt settlement. It also depends on the size of your debts, and the deals your debt settlement firm can secure for you. Complete debt settlement often takes four to five years.

Can I Negotiate Credit Card Debt Settlement on My Own?

Yes, you can do DIY debt settlement, but that doesn't mean it's the best idea. If you are an expert negotiator with knowledge of how debt settlement works and loads of time and patience, you can contact your creditors directly, one by one, and obtain written agreements covering all the legal terms of your settlement deal. Or you can work with a trusted debt settlement company like ClearOne Advantage and let it do all the work on your behalf.

A debt settlement company has experience with the negotiation process and can provide support throughout, including creditor communication and settlement documentation.

What to Look for in a Debt Settlement Company

Your debt settlement company should have a good reputation. Look for a high rating on TrustPilot and positive client feedback on the services debt settlement companies offer. Make sure that you opt for the services of an entity that has helped thousands of customers already.

Contact the debt settlement company and after your initial conversation, ask yourself these questions.

- Is this debt settlement company committed to working out the best solution for my situation?

- Does it possess the tools and resources to help me achieve my goal of freedom from debt?

- Does it have a team of skilled negotiators capable of obtaining a good debt settlement deal for me?

- Can I afford the services of this debt settlement company without further exacerbating my financial situation?

Let ClearOne Advantage Help You Settle Credit Card Debt

By partnering with ClearOne Advantage, you secure the services of a dedicated team of professionals whose goal is to negotiate the best possible deal on your behalf.

- ClearOne Advantage does not charge you upfront fees and offers personalized plans to suit your needs.

- Our Certified Debt Specialists make sure that you understand all the details of your debt settlement plan before you commit.

- We give you access to an online portal through which you can track your debt settlement progress in real time.

- Our expert negotiators have years of experience working out the best settlement deals for our clients.

- Our Client Relations Specialists support you throughout the debt settlement process to keep your efforts on track.

- https://www.nerdwallet.com/credit-cards/studies/household-debt-study

- https://www.federalreserve.gov/publications/2025-economic-well-being-of-us-households-in-2024-savings-and-investments.htm

- https://www.cars.com/articles/how-much-is-the-average-car-repair-bill-1420694859724/

- https://www.clearoneadvantage.com/documents/Dobbie_Report.pdf