How Bankruptcy Works and What to Expect

If you're among the millions of Americans overwhelmed by credit card debt, you may be considering bankruptcy. This can clear debt quickly but significantly impacts your credit. Fortunately, it's not the only option. Read on to learn more about bankruptcy and how it compares to other debt relief options.

Here are a few important questions to consider about bankruptcy.

- What is bankruptcy?

- What are the types of bankruptcy and how do they work?

- Who should declare bankruptcy?

- What are the alternatives to bankruptcy?

- Is debt settlement a good alternative to bankruptcy?

- What are the pros and cons of bankruptcy?

- Does bankruptcy relieve you of all debt?

- How does bankruptcy impact your credit score?

- How to avoid bankruptcy with a debt settlement plan.

What Is Bankruptcy?

Bankruptcy is a legal process that allows debtors to repay a portion of their debts, or to have all debts forgiven. Through bankruptcy, debtors can gain relief from most of their debts, although there are some exceptions. Bankruptcy typically does not offer a reprieve from:

- Child support obligations

- Student loans

- Certain types of personal income taxes

- Criminal fines

Bankruptcy aims to give debtors in a hopeless financial situation a way to start over. It is not designed to be an easy or attractive way of avoiding debt repayment. It comes with significant costs and restrictions. The most obvious cost of bankruptcy is credit score damage. People who opt for bankruptcy should know that it is unlikely that they will be able to obtain future loans at a favorable rate for many years after filing bankruptcy.

State law determines the exemptions associated with bankruptcy, meaning the assets the bankruptcy filer may keep after liquidation. Exemptions typically cover one's house, clothes, and first vehicle. Most states do not exempt second vehicles, collectibles, antiques, etc. The filer may have to forfeit such assets to the trustee.

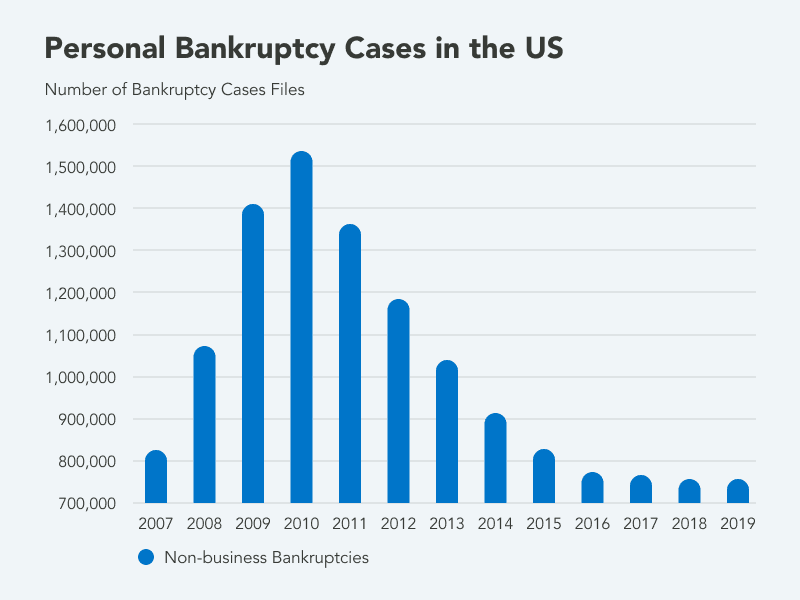

Bankruptcy by the Numbers

Since 2007, millions of Americans have chosen the path of personal bankruptcy to address their debts.

Usually, people facing extreme financial hardship consider bankruptcy as a last resort. Bankruptcy impacts your credit score and can stay on your credit report for 7 to 10 years depending on the type of bankruptcy for which you qualify.

What Are the Types of Bankruptcy and How Do They Work?

The two most common personal bankruptcy filings are Chapter 7 or Chapter 13.

How Chapter 7 Bankruptcy Works

When a debtor files for Chapter 7 bankruptcy, an 'automatic stay' comes into effect. This 'stay' lasts until the end of the bankruptcy process and it prevents creditors from making any collection efforts. It also denies creditors the possibility to sue the debtor.

The bankruptcy filing notice pops up on the credit report of the debtor just as quickly as the 'stay' goes into effect. This 'black mark' remains on the credit report for up to 10 years in the case of a Chapter 7 bankruptcy. Record of the debts that the bankruptcy proceedings discharge remain on the debtor's credit report for up to seven years as well.

Typically with a Chapter 7 filing, it should not take longer than three to four months for your debts to be discharged.

To qualify for Chapter 7 under the provisions of the 2005 BAPCPA, the monthly income of your household needs to be under the state median for households of similar size.

After a Chapter 7 debt discharge, you may not file another Chapter 7 bankruptcy for eight years.

How Chapter 13 Bankruptcy Works

Chapter 13 is more about debt consolidation than debt discharging. The debtor submits a financial reorganization and debt repayment plan. They proceed to make monthly payments under the plan the court approves, in a consolidated manner.

It is the job of the impartial trustee to distribute the payments to the debtor's creditors.

The length of the repayment plan is three-to-five years. The repayment plan is not lenient. It aims to pay creditors at least as much as they would receive under other types of bankruptcy. It also does not shy away from seizing 100 percent of the filer's disposable income for repayments. Chapter 13 bankruptcy may stay on your credit report for up to 7 years.

Eligibility for Chapter 13

To be eligible for Chapter 13, you need to fulfill a series of requirements.

- You need to undergo credit counseling before filing.

- Your individual unsecured debts cannot exceed $526,700

- Your individual secured debts cannot exceed $1,580,125

- You need to submit an income/monthly expense report to the court.

- You have to list your creditors as well as the amounts you owe them.

When Is Bankruptcy an Option?

The person who typically resorts to this debt resolution method is in a dire financial situation. This means that he or she:

- Has massive debts and no hope to repay them.

- Is behind in mortgage payments.

- Is in danger of foreclosure.

- Is being pressured by collectors.

- Cannot budget his/her way out of debt, even after the addition of a second job.

Remember that bankruptcy may not be the best solution in your case. Discuss your options with a qualified bankruptcy attorney before even thinking about filing.

What Are the Alternatives to Bankruptcy?

Other alternatives may be debt settlement, debt consolidation, credit counseling, and debt reduction by your own means. Credit counseling and debt consolidation loans are generally chosen by people with a smaller debt load and good to excellent credit. These methods of debt relief may not work for those with a larger amount of debt who are considering bankruptcy.

Is Debt Settlement a Good Alternative to Bankruptcy?

Debt settlement may be a good choice for those hoping to avoid bankruptcy.

Unlike bankruptcy, debt settlement does not require a court filing. You are not required to retain an attorney or additional financial counseling. You do not pay any upfront fees. While you make payments, you may not have to repay your debts in full.

Your creditors settle for less because they know you have left open the option of bankruptcy, which could leave them with little chance to collect your debts.

Learn more about bankruptcy vs. debt settlement.

| Debt Settlement | Bankruptcy | |

| Credit Score | No set requirement | No set requirement |

| Qualifications | At least $10,000 in unsecured debt and regular income | Must document income and expenses for court. Typically must have no disposable income. Debt usually >50% of your annual income. Income below the median level for your state. |

| Upfront Fees | $0 | $500 to $3,500 - court filing and attorney fees can vary |

| Financial Benefits | Provides short-term relief with a low monthly payment, and long-term relief with avg. term of 24-51 months | Forgives most unsecured debts, like medical bills, credit card debt, and personal loans. |

| Credit Impact | Significant, but not as bad as bankruptcy, which has the biggest impact to credit according to the FTC | Severe impact lasting up to 10 years |

| Other Factors to Consider | May reduce original debt load by half (exclusive of fees) | Typically need to be current with tax filing. Must undergo credit counseling 180 days before filing. Irrevocable. |

Pros and Cons of Bankruptcy

Although bankruptcy is sometimes the only answer for someone in a desperate financial situation, it should not be entered into lightly. Before deciding to go this route, you should make sure you have exhausted all your other debt relief options. Debt Settlement may be a viable alternative and a ClearOne Advantage Certified Debt Specialist can walk you through your options and help you decide what may be the best choice for you. Below, we've outlined some of the pluses and minuses of bankruptcy:

Pros

- You gain protection from debt collectors and creditors for the duration of the bankruptcy proceedings, in the form of a 'stay.' (Chapter 13, in particular, allows you to keep your assets during the stay.)

- The payment plan for Chapter 13 may be able to include legal fees.

- 95% of Chapter 7 cases are completed successfully.

- If your Chapter 13 case is dismissed, you will have to wait 180 days before you are allowed to file again.

- With a Chapter 13 filing, you have the flexibility to adjust your court-approved payment plan during the case, instead of being locked into the original terms.

Cons

- Chapter 7 requires a means test and there are stringent qualifying requirements.

- Both Chapter 7 and Chapter 13 bankruptcies have a high negative impact on your credit score that lasts for 7-10 years.

- Filers likely need legal representation. The process is costly and intricate. Attorney fees can cost thousands of dollars.

- After filing for Chapter 7, you cannot file again for 6 years.

- Chapter 13, in particular, carries a lower success rate than Chapter 7. Success rates vary from 40-70%.

- For Chapter 13 filings, the trustee will renegotiate the payment plan if the financial situation of the debtor improves.

Source for bankruptcy success rates: American Bankruptcy Institute

Does Bankruptcy Relieve You of All Debt?

A Chapter 7 bankruptcy relieves you of all qualifying unsecured debt. There are certain exemptions such as child support obligations, criminal fines, and student loans, to name a few.

A Chapter 13 bankruptcy requires you to repay at least as much of your debt as you would through a Chapter 7 bankruptcy.

On the other hand, with debt settlement, all of your creditors do get repaid at least a portion of what you owe. Before taking a drastic step like bankruptcy, you owe it to yourself to consider ClearOne Advantage debt settlement as a viable option.

How does Bankruptcy Impact your Credit Score?

Bankruptcy significantly impacts your credit and stays on your credit report for 7-10 years.

A debt settlement plan with ClearOne Advantage will also have a negative impact on your credit score, but that impact may not be as severe as the impact of bankruptcy, which should be considered as a last resort.

How to Avoid Bankruptcy with a Debt Settlement Plan

Debt settlement programs can be lengthier than bankruptcy, but many consumers consider it a better option than filing for bankruptcy.

ClearOne Advantage and our Certified Debt Specialists are here to help take care of the debt relief process for you. Give us a call at 888-340-4697. While our goal is to get you out of debt in a reasonable amount of time with a payment you can afford, we are also committed to providing you with the support, tools, and resources to help you gain control of your finances.

Disclaimer: ClearOne Advantage is not a law firm and does not provide legal advice. If you are considering bankruptcy you should consult a licensed attorney.