If your credit card balances have been harder to keep up with lately, you may notice that the impact goes beyond your monthly payments. Debt can influence your stress levels, your relationships, and your long-term plans. Understanding these effects is the first step toward deciding whether debt relief might be right for you.

Key Points:

- Debt can affect your stress levels, relationships, and overall wellbeing.

- Ongoing balances may contribute to anxiety, sleep issues, or feeling mentally drained.

- Financial pressure can sometimes show up physically, from headaches to changes in appetite.

- When debt feels overwhelming, it’s common to avoid looking at statements or putting off decisions because acknowledging your debt is uncomfortable.

- The good news: exploring debt relief options may help you create a clear plan and start moving forward with more confidence.

According to Bankrate, 47% of Americans with credit cards carry a balance from month to month, and Experian reports that the average American holds 3 credit cards and carries an average credit card debt of $5,897. If you aren't paying your balance in full each month, your debt can add up quickly.

The Financial Cost of Credit Card Debt

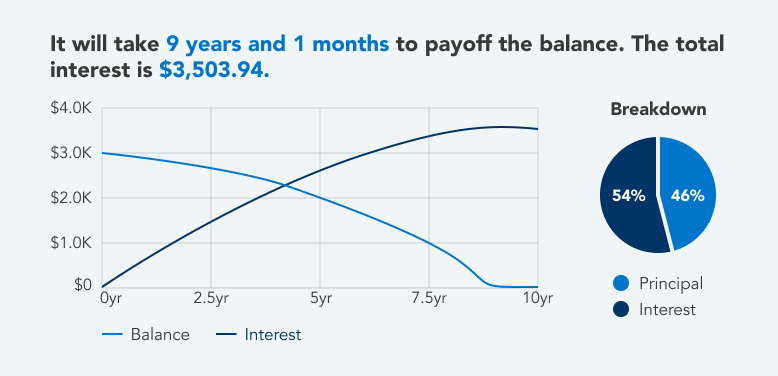

The cost of credit card debt can add up quickly. If you carry a $5,000 balance on an account with a 15% APR and you make minimum payments on that account, it will take you five and a half years to pay off the credit card. Over that time, you would pay about $2,343 in interest alone.

(Source: Calculator.net)

How Credit Card Debt Impacts Your Life Outside of Finances

Manageable debt (debt that can be handled with budgeting techniques) does not have a noticeable negative impact on the lives of most people. In fact, some Americans view secured debt such as mortgage loans or auto loans as normal expenses.

However, there is another kind of debt that has a much different impact. When your balances become difficult to keep up with, the effects may extend beyond finances and start affecting your mental, emotional, and physical wellbeing.

Debt-Related Stress, Anxiety, and Depression

Stress is a common response when your debt feels difficult to manage. If you've missed payments, your credit score may decline. This can make it harder to access new credit, which may add to the pressure you're facing.

Over time, ongoing financial strain can affect your mood and energy levels, leading to depression. When money concerns take up mental space day after day, it can become harder to focus, stay motivated, or feel optimistic.

Chronic stress may also show up physically, from changes in appetite and sleep patterns to difficulty concentrating.

Physical Effects of Uncontrolled Debt

Financial stress may also take a toll on your body, leading to:

- Debilitating headaches

- Upended sleep patterns

- Difficulty with concentration or focus

- Substance use

- Changes in appetite or weight

- Neglecting self-care

Debt-Related Social and Family Problems

Debt can influence family life in practical ways. It may limit your housing choices, delay certain goals, or make career changes feel harder to pursue. In some cases, families may postpone saving for education or retirement while focusing on paying down balances.

Debt can also cause strain in your relationship. According to a 2025 survey from Debt.com, 42% of divorced couples say that credit card debt played a role in the breakdown of the marriage.

Debt Denial & Avoidance

One of the most harmful ways debt can impact your life is by keeping you stuck in denial or avoidance. When debt feels overwhelming, it can be incredibly hard to accept that it’s become a problem, and even harder to know where to start.

Avoidance is often part of this cycle. If your balances feel too stressful to face, it may feel easier to put off dealing with them, hoping the situation will somehow improve on its own. While this response is understandable, ignoring the problem usually provides only temporary emotional relief and can allow the debt to grow over time.

Here are a few signs you may be facing debt denial:

- You know you have a debt issue but feel paralyzed by fear, and struggle to make concrete plans to get out of debt.

- You hope that things will just “work out” without changing your spending or repayment habits.

- Looking at your balances feels overwhelming, so you avoid checking credit card statements.

- You find yourself opening new credit cards without taking care of the balances on your existing credit card accounts.

Over time, avoidance can make debt feel even more unmanageable. The good news is that recognizing this pattern is often the first step toward regaining control. If you see yourself in these signs, seeking debt relief support can help you move forward with clarity and confidence.

ClearOne Advantage Provides Real Credit Card Debt Relief

No matter how stressed you are feeling, there are credit card debt relief options available to you.

ClearOne Advantage has a team of debt relief professionals who are standing by to help you. It all starts with a simple phone call. Call 888-340-4697 to speak with one of our Certified Debt Specialists, who will help you design a plan that fits your budget and addresses your needs.

The data and statistics referenced come from multiple credible resources that are cited throughout. ClearOne Advantage makes no representations or warranties regarding the accuracy of information from these resources and is providing this content for informational purposes only.