Debt has become ingrained in American culture. Today, few of us can imagine a car without payments, a house without a mortgage, or a college student without a loan. In addition to these debts, Americans are also carrying a significant amount of credit card debt.

How Much Credit Card Debt Is There?

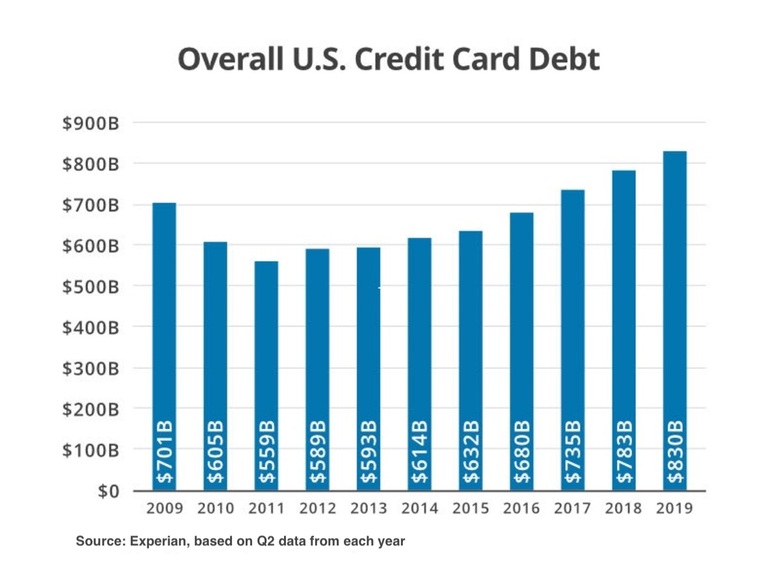

According to recent data from Experian, Americans have $830 billion in credit card debt, an amount that has been rising steadily for several years.

Experian’s research also found that 61 percent of Americans have at least one credit card, and the average number of credit cards per person is four. Meanwhile, the average balance carried on credit cards is $6,194.

A Harris Poll survey of 2,076 U.S. adults conducted in the third quarter of 2019 found that the average total amount of revolving credit (which refers to carrying a balance on your credit card month to month) amounted to $7,104. Further, the average cost of this debt in interest is more than $1,100 per year, per household.

ValuePenguin research indicates that amount is even higher. For households that actually carry a credit card balance from month to month, Valuepenguin's research found that the average credit card debt was $9,333 across all income levels.

Digging deeper, researchers found that amount changes significantly based on the net worth of a household. Generally, the larger the net worth of your household, the larger balance you carry on your credit card. For instance, households with a net worth between $5,000 and $9,999 carried revolving credit card average balances of $4,912 while households with a net worth between $50,000 and $99,999 carried revolving credit card average balances of $6,776. The exception to this trend was households with a negative to $0 net worth, which carried revolving credit card average balances of $10,307.

How Does Credit Card Debt Accrue?

There are a number of factors that contribute to credit card debt. Perhaps the most obvious of them is impulse spending, but the reality is that impulse spending may account for less of the problem than you may think.

Investopedia spotlights another factor, noting that the average household income over the past twenty years has failed to keep up with the average pace of inflation. That means that your dollar does not go quite as far as it used to toward paying your living expenses, which in turn may mean that you begin to rely on your credit cards to care for some of those living expenses.

Other factors include a steep rise in medical costs, education costs, and even housing costs. Recently, economic difficulties resulting from the COVID-19 pandemic have put some families under additional financial pressures and led to increased reliance on credit cards to meet everyday needs.

Then, there is the matter of financial illiteracy. Though many people have credit cards, fewer understand how those cards work in terms of interest calculation, cash advance fee calculation, and minimum payment calculation. This lack of financial knowledge leads to poor decision-making, which in turn leads to the amassing of credit card debt.

How Can You Keep Credit Card Spending under Control?

The best way to keep credit card spending under control is to limit the number of credit cards you own and limit the use of them. Try to only charge as much as you can reasonably pay off every month and avoid carrying a balance from one month to the next.

If that is not possible, look for a credit card with no annual fee and a low APR and keep a strict watch on your purchases, limiting them to essential purchases only.

Some people find it useful to keep their credit cards in a place that is not easily accessible. If you do not have your credit card with you when you're window shopping, you may be less likely to make an impulsive purchase. Another tip from financial experts is to delay making a major purchase on your credit card for at least one day, which gives you time to truly consider your options and decide if you really want to carry a balance on your card.

If you already have a small balance on your credit card, pay more than the minimum payment each month until the balance is reduced substantially. If possible, pay at least double the minimum payment to see faster results.

How Do You Get Out of Serious Credit Card Debt?

What if you owe more than a small amount on your credit cards? It is not uncommon for some households to owe as much as $10,000 to $125,000 in credit card debt. If you are in that situation, you may feel that you will never get free from your credit card debt.

You're not alone. In one Nerdwallet study, 10 percent of survey participants estimated it will take them over 10 years to get out of credit card debt, and an additional 11 percent do not think they will ever pay off their credit cards completely.

However, you do not have to remain in debt for that long. You can break free of credit card debt in a much shorter amount of time with some professional help. Talk to a ClearOne Certified Debt Specialist at 866-481-1597 to understand the debt relief options you have at your disposal.