How to Become Debt Free

Becoming debt-free starts with a clear plan and consistent action. It is not about quick fixes or temporary solutions. It means taking an honest look at your finances, setting a structured repayment strategy, and staying committed to the process. When you stick to the plan and have the right guidance, reducing your debt becomes more manageable. ClearOne Advantage provides the support and foundation you need to take control of your finances and work toward lasting financial stability.

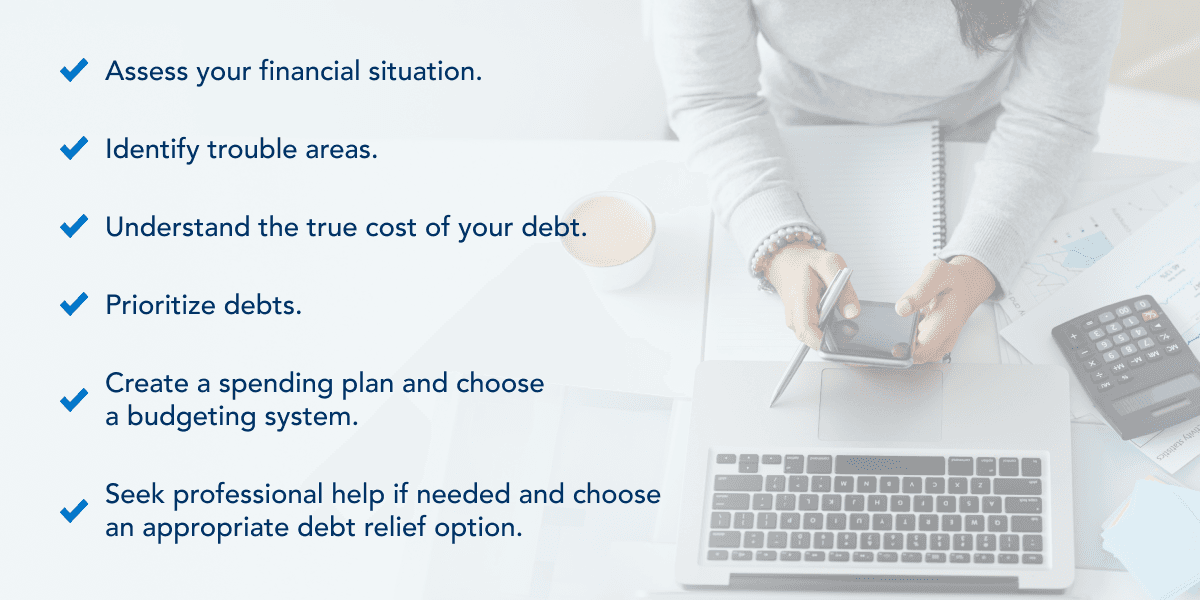

Steps to Becoming Debt-Free:

Let's look at each of these steps in a bit more depth.

Step One: Assess Your Financial Situation

How you address your debt depends on your current circumstances. You may have already taken steps to improve your financial situation, but knowing where you are right now will help you identify what you need to bridge the gap between where you are and where you want to be financially.

If you are having trouble with this, or any steps in the process, we recommend consulting with a ClearOne Advantage Certified Debt Specialist. We have helped thousands of people develop plans to improve their finances and defeat their debt and can help walk you through the process.

Read More: Practical Tips for Debt-Free Living

Step Two: Identify Trouble Areas

Everyone handles money and juggles finances according to their own set of beliefs and attitudes. Some of those beliefs may be handed down from parents or other respected people in our lives, but when you decide to tackle debt, it's good to take a step back and examine your financial belief system. You may find that some of your attitudes or beliefs about money matters are contradictory to your goal of ridding yourself of debt.

Knowing your trouble areas is the first step toward eliminating them. It also helps to have a good understanding of where your debt originates.

The average American consumer is likely burdened with debt originating from:

- Mortgage Loans

- Home Equity Lines of Credit

- Auto Loans

- Student Loans

- Credit Cards

- Unsecured personal Loans

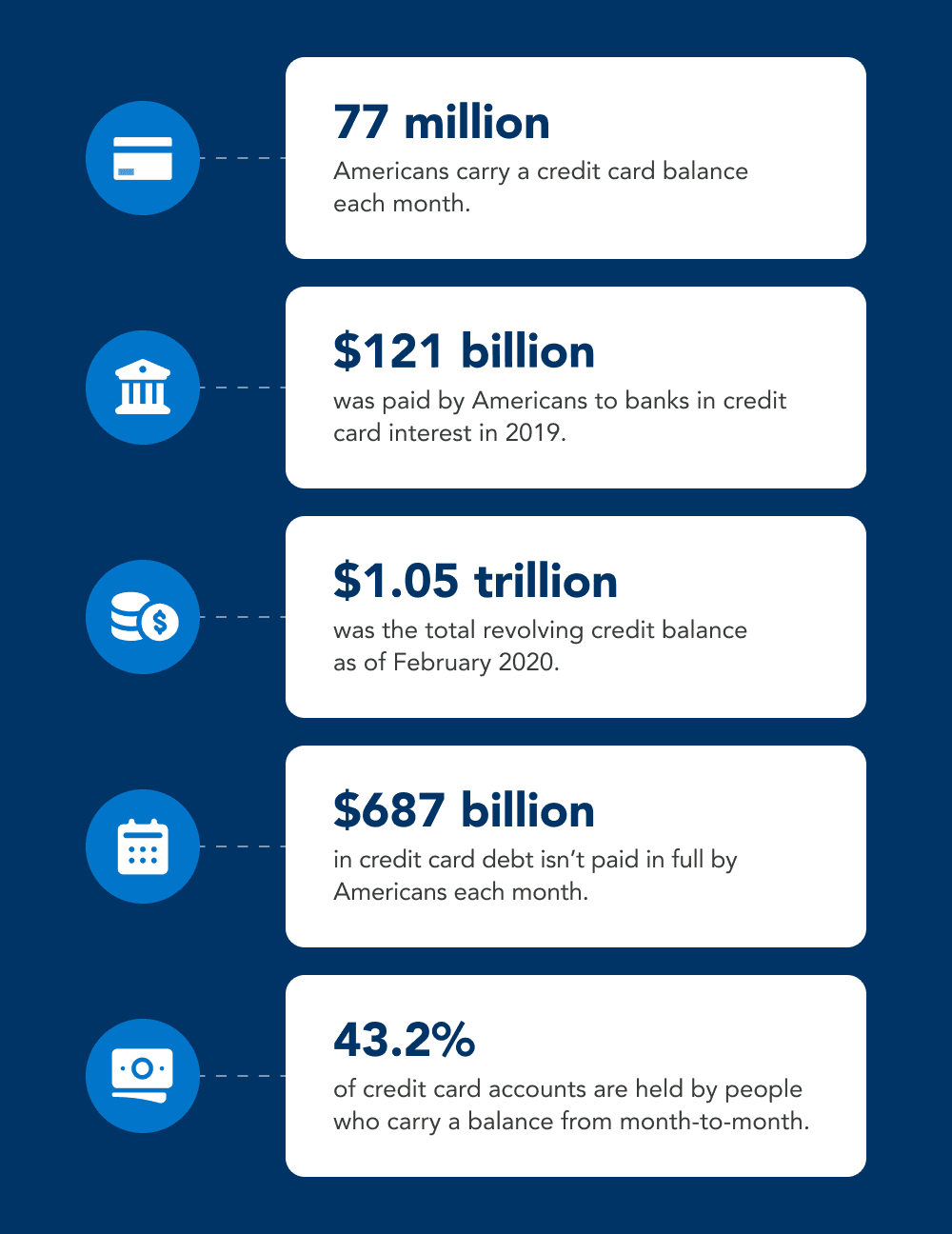

Credit Card Debt Statistics

Unexpected expenses like medical bills, travel, and everyday necessities, along with impulse purchases on credit, can quickly lead to overspending. When you're only able to make minimum payments, it becomes harder to build lasting financial stability.

(Source: Magnify Money)

Step Three: Understand the Cost of Debt

Exactly how expensive is debt?

Consider the following hypothetical example. You have a debt of $26,000 with 18 percent interest and you pay the 3 percent minimum amount every month.

1st Year of Payments:

At the end of your first year, you will have paid $7,965. After interest charges, you will have reduced your principal by $3,982, for an owed balance of $22,018.

4th Year of Payments:

By the end of your fourth year, you will have paid $26,443, which is $443 more than your original debt amount. Your owed balance would still be $12,778!

Step Four: Prioritize Debts

If you cannot meet your monthly debt obligations and you need to decide which debts to pay, the debt your creditor is most aggressively trying to collect is not your top priority.

Your top priorities are the roof over your head, your car, and your necessities. Secured debt is your greatest priority. Defaulting on these types of debts can jeopardize these assets.

Follow this list of priorities instead.

- Cover your necessities such as food and inevitable medical expenses.

- Keep up your mortgage/rent payments.

- Try to keep your utilities going.

- If your vehicle is a necessity, keep up your car loan and insurance payments.

- Keep up with child support. Missing such payments may land you in jail.

- Pay your income taxes.

- Take care of student loan payments.

- Missing such payments may rob you of tax refunds and federal benefits you may enjoy.

- Address unsecured debts, such as credit card debt.

Step Five: Create a Spending Plan and Choose a Budgeting System

A spending plan will help you get started with your credit card relief in three ways.

- It will give you peace of mind and establish healthy spending habits.

- It will tell you exactly how much money you have at your disposal to address your debts.

- It will also tell you how much you need to get out of debt for good.

Setting up a budgeting system may be as simple as grabbing a pen and some paper. You can also use dedicated apps or spreadsheets to help. Break your expenses into three categories.

- Fixed committed expenses (like your mortgage/rent)

- Variable committed expenses (like groceries and utilities)

- Discretionary expenses (gym memberships, cable service, cell phones, etc.)

Step Six: Seek Professional Help and Choose a Debt Relief Option

Your current financial situation determines whether you need professional help with debt resolution or not. Ask yourself some questions.

- Do you use credit cards to fill the gap between your spending and monthly income?

- Do you only pay the minimum amount on your credit cards or make payments late?

- Have you “juggled” credit cards, opening new ones, and transferring balances?

- Are debt collectors pressuring you?

- Have you experienced a significant recent drop in income?

- Do you include credit cards in your budgeting?

- Do you buy necessities on credit?

- Have you maxed out your credit cards?

If your answer is “yes” to more than a couple of these questions, you likely need professional debt relief help.

Contact a ClearOne Advantage Certified Debt Specialist at 888-340-4697 to help you determine what the best debt relief option may be for you.

ClearOne Advantage Can Help

You do not have to take all of these steps on your own. ClearOne Advantage can help you with each of these steps. Our Certified Debt Specialists can discuss your current financial situation with you to help you determine the best plan for going forward and getting out of debt within a reasonable amount of time. With some diligence, perseverance, and help, you can realistically defeat debt.

Take a proactive step to eliminate the stress of debt from your life now. Call one of our Certified Debt Specialists and get a personalized debt relief plan today.