In most cases, you do not inherit debt from your parents or other family members. When someone passes away, their debts are typically paid from their estate, not from the personal finances of their children or heirs.

Read More

In most cases, you do not inherit debt from your parents or other family members. When someone passes away, their debts are typically paid from their estate, not from the personal finances of their children or heirs.

Read MoreTopics: Financial Wellness

If you’ve been shopping online recently, you’ve probably seen an option to split your purchase into smaller payments using services like Klarna or Affirm. This “Buy Now, Pay Later” option can make purchases feel more manageable in the moment. But you might be wondering whether it’s actually a good financial move.

Read MoreTopics: Financial Wellness

For some, earning rewards through churning is an attractive option. For others, frequent credit applications may mean lower credit scores and credit card debt. In many cases, though, the need for constant credit card payoff can lead to financial strain.

Read MoreTopics: Credit Card Debt

If your credit card balances have been harder to keep up with lately, you may notice that the impact goes beyond your monthly payments. Debt can influence your stress levels, your relationships, and your long-term plans. Understanding these effects is the first step toward deciding whether debt relief might be right for you.

Read MoreTopics: Credit Card Debt

When you are dealing with debt, increasing your income often feels like the most logical solution. More money can mean faster payments, less stress, and a quicker path out of debt, but only if it is used strategically.

Read MoreTopics: Debt Relief

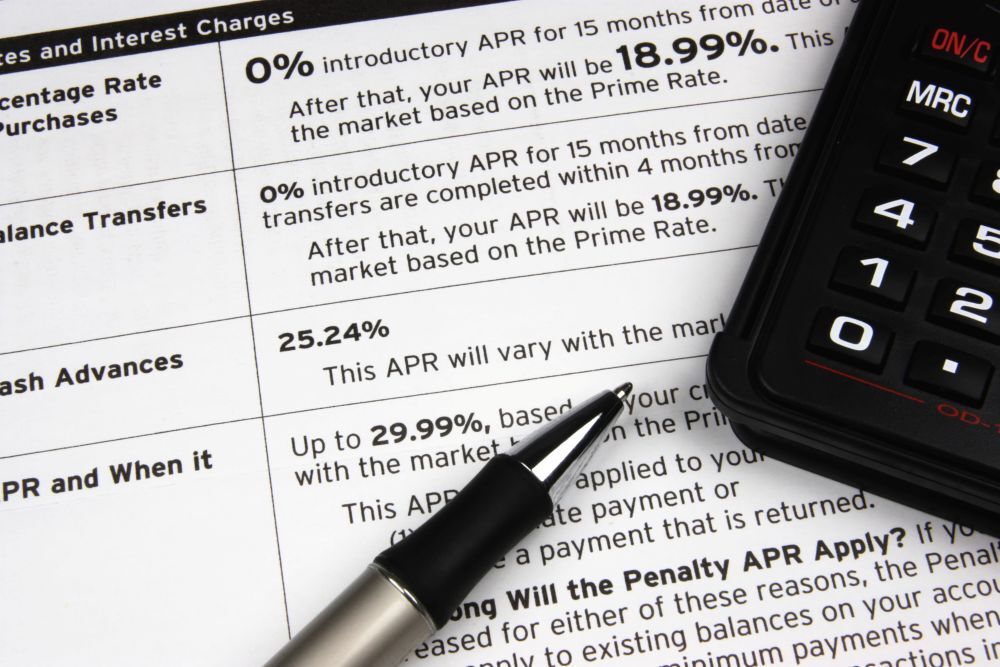

There is growing discussion in national media and in Congress about proposing a 10 percent cap on credit card interest rates to ease the burden of high-cost borrowing. Headlines highlight potential savings for consumers, but often leave out important details about how a cap would actually work and who would benefit most.

Topics: Credit Card Debt

Debt settlement saves you money by shaving off a set amount of your credit card principal. It’s a viable solution when you feel that the debt amount on credit cards you have accumulated is simply unmanageable on your current income.

You may, however, owe taxes on the money you save this way. In many cases, it is considered income, and you are required to report it as such to the Internal Revenue Service (IRS). For example, if you owe $25,000 in debt and your creditors agree to settle personal loans for $15,000, you will be taxed on the remaining $10,000.

Read MoreTopics: Debt Relief

Debt-free living can feel out of reach, but many people achieve it with the right plan and consistent habits. Becoming debt free isn't about perfection; it's about understanding your finances, making intentional decisions, and sticking with a strategy that works for you. The practical steps below can help you build a lasting debt-free lifestyle and take control of your financial future.

Read MoreTopics: Financial Wellness

Most people need to borrow money at some point, whether for a car, a home, an emergency, or a major purchase. Yet despite how common borrowing is, many of us never learn how to borrow safely or choose the right type of loan. If your credit score isn’t perfect, borrowing can feel even more confusing. The good news: there are safe, responsible ways to borrow money even with less-than-ideal credit. Here’s how to navigate your options and protect yourself in the process.

Read MoreTopics: Financial Wellness

Every January, New Year’s Resolutioners flock to gyms across the U.S. to get in shape for the new year. Doesn't it make sense to pay as much attention to your financial fitness as your physical fitness?

Read MoreTopics: Financial Wellness

©2026 ClearOne Advantage, All rights reserved.

ClearOne Advantage is a registered service mark of

ClearOne Advantage LLC.